Critical decision factors for an investment into closed-end funds

Critical decision factors for an investment into closed-end funds

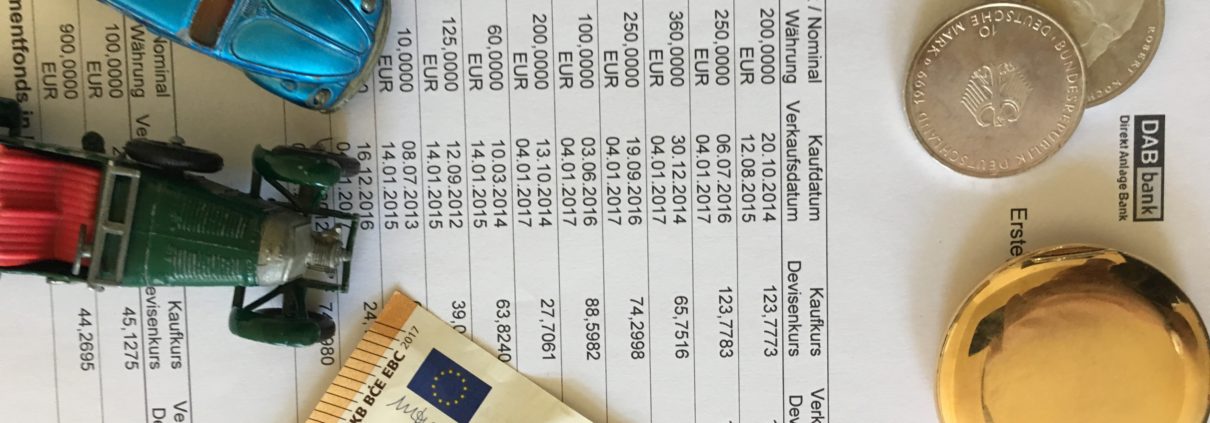

On the occasion of a risk diversified investment strategy but also for reasons of pensions investors often have to take decisions of an investment into a closed-end fund. Usually in such a case, a limited partnership is founded with the purpose to acquire special kinds of assets, for example real estate, plans, ships or containers. Such an asset is hold and rented by the partnership for a certain time period, regularly at least 10 years. After this period the asset will be sold by the company to a third party. For reasons of financing the acquisition of the asset, funds are collected from the interested investors as the future limited partners of the company. The limited partners are hold liable for their contribution agreed on. In case of a default of the investment a total loss of the contribution can arise. This means that the invested money can be completely get lost. However, there is no obligation which is agreed on in the partnership agreement of the limited partner to finance further funds.

Under economical aspects the fund prospects to the investors periodic payments of dividends. However, in this context it has to be taken into account, that generally the dividend policy of the fund provides only the initial capital payment of the investor or parts of it for continuous repayments during the lifte time of the closed-end fund. These capital repayments have no tax effect for the investor which means that the payment will not be taxed as fiscal income. However, every capital repayment does increase the amount of the future capital gain resulting from the sale of the asset hold by the closed-end funds („exit“).

Apart from the prospected further capital gain as consequence of the exit which could be even so subject to various financial risks, the investor should also consider other aspects for his investment decision. These include not only the life time of the fund, but also the potential requirement of an agio payment, the amounts of provided periodic dividends as well as the calculated annual cost of the management of the fund. The latter case concerns also the external fees of the tax advisor, various lawyers and the public certified accountant of the fund. Additionally, the investor has to consider, that during the life time of the close-end fund the exit of a limited partner from the partnership on the basis of the fair value of the participation ist generally not possible. Even so a second hand market for funds participation does exist, frequently, a sale without any relevant discount is not possible. As a consequence, the original capital payment is bound de facto to the partnership over the whole life time of the fund.

It is normally recommend to involve a certified public accountant, a tax advisor or a specialized lawyer to check the investment before signing the partnership agreement. This includes especially the essential points of the shareholder agreement (e.g. succession plan rule, tax character of the fund) but also the reliable calculation of the economics of the fund with special regard to the advantageousness e.g. in relation to the investments in traded stocks.